Education Fees, The necessary Devastation

- paulnkumbula

- May 25, 2020

- 5 min read

Updated: Nov 29, 2020

Introduction

“Educational fees can be unbearable and a heart breaking cost of any salary or other income earner. It is one of the top issues that leads to people getting into debt and depression if not carefully managed.”

Over the years of my adult working life i regret one thing. The failure to have realised earlier the power of saving for future educational needs despite being a low income earner. Many people rank education as the top most priority of what they will ever do in life either for them or to people they support in life. It is therefore vital that it (#education) is given the best attention ever.

Savings That Could have Saved You

If you are reading this and asking your self what is the whole purpose of saving when what you earn is not really enough to be left with anything to save? Well, i also asked my self the same sane question like you did but tragic enough i never seemed to know anything about saving. In fact i had a crazy theory that the more i spent the more money came back to me. i really was impatient when it came to spending and for some reason i thought that people who save are just greedy people who are unconcerned about needs that really matter in life.

Today, looking back at the situation i was in at that time were it was practically impossible for my monthly earning to support for my educational and other day to day needs as they came by, its regrettable to learn of the many options that i could have utilised then. I learnt the hard way that is through experience which anyone else could avoid freely today by applying some helpful and practical tips in this article.

If there is advise i can offer to someone wanting to commit to future educational needs either for their children, siblings or other relatives is to avoid the move if to them it seems practically impossible to put in place a clear plan of how it can be achieved.

One vital lesson to learn is that nothing in life works out by itself unless if you believe in miracles (even as we know faith without works is useless) and the reality of getting into the most stressful and lifetime debt is real everyday through the lifetime decisions of many people today.

As the saying goes, "its easier to spend than to earn", the reason anyone needs to be careful whenever it came to spending decisions especially on college or university education.

So now how do we ensure that we create a position that can help us not to worry about our educational needs as they become due for payment?

If you look at todays most sought after option when it came to financing education is debt. In Zambia, It is expensive to borrow small amounts of money and borrowing may not solve your money problems over time and many risk being in a debt trap and it is the last path you would want to use. The second most sought after option is insurance. In as much as insurance is a better option as compared to debt it might not be the best next alternative of financing education due to certain limitations and challenges in claiming for your funds once your insurance policy period elapses. I have seen a lot of many insurance educational policies from prominent insurance companies in Zambia that takes too long too to be claimed and how they don't factor in the value of money over time. Its risky to open an educational insurance policy in Zambia and if you want to know more about our insurance companies review in Zambia you can read more on this article here.

So what's the best way out? Firstly, as an income earner you need to realise that understanding and valuing the culture of saving is gold. You need to begin with a mind of taking education as an investment and not just as any burdensome bill. Therefore if you take education as an investment then choosing the best kind of savings option is key. I will illustrate this with an example.

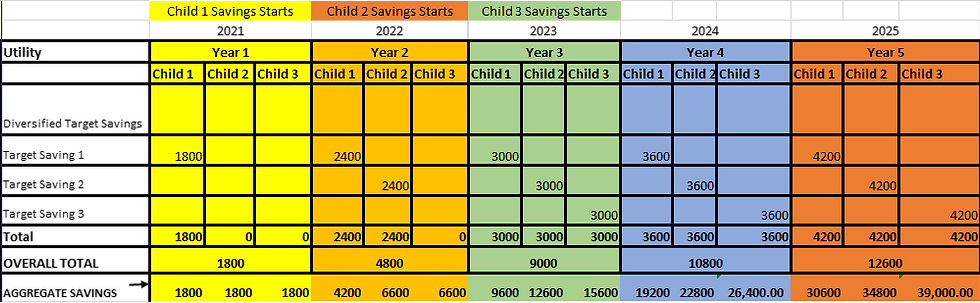

Say you are a salary earner who has three children, one who is seven years old and in grade 2, the second who is 4 years old and in Pre-grade and the last born who is 2 years old and in preschool. Firstly, as a parent you have already begun to spend on their education and say you are spending K2,000 monthly for all of them with a total educational spending of K24,000 yearly. So you need to design an investment plan or strategy that will ensure that you still keep track of the current obligation of K2,000 and also enable you save monthly towards their future education at Mid Grade (9th and 8th Grades), High School and at college/university. To explain this better here is a model that we shall use to illustrate the kind of strategy to use over a period of about 10 years.

Target Educational Savings from Year 1 - 5

Target Educational Savings from Year 6 - 10

Beginning in year 1, 2 and 3 (2021-2023) by saving for Child 1, 2 and 3 with a monthly amount of K150 in Year 1 for Child 1, K200 in Year 2 Child 2, 250 in Year 3 for Child 3. Based on this model, if you strictly follow this plan you shall save for the first child up to K15,000 and a total of K53,000 for all the children in year 6 which amazingly enough to give some quality education even if the current price for one child may double after six years (K12,000 per year). If the model may carry on for the first child until year 10 when the child finally completes the 12th grade, a total of K57,000 is still available to be spent on her/his college or university education even if todays university yearly fees may double (K52,000). This model position has been based on a very conservative starting amount of just K150 savings per child per month. Now if depending on someone's income this could be increased to say K300 then the whole model dramatically doubles and changes significantly. Remember that with this model we have not filled anything under diversified target savings which can be a line were you enter the growth of other kinds of investments such as educational investment in stocks or shares, livestock, real estate, savings interest bearing account etc which can assist in growing the investment faster

Comments